Investing in drawdown: an innovation gap?

The 2014 budget removed restrictions on how retirees use their pension pot and since April 2016 all defined contribution retirees have been able to spend or invest their pension funds as they see fit, with or without financial advice. This has opened up new possibilities for pensioners but has also brought with it increased complexity in terms of the issues that retirees need to grapple with to decide what to do with an asset that is usually their second biggest after their homes.

What do customers want?

Initial expectations of a flurry of new innovative products to service this market have, so far, mainly failed to materialise. This is primarily because life companies have been concentrating on embedding the new Solvency II regulatory regime and ensuring that administration systems are in place to allow the necessary initial fund transfers to take place.

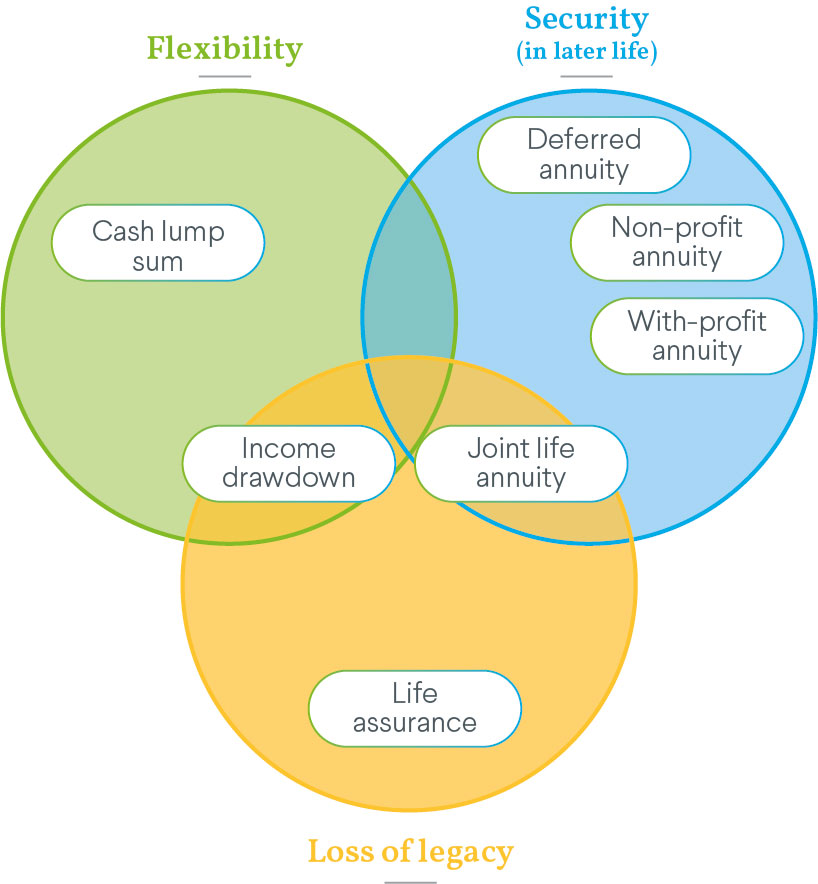

Another barrier to new product development has been the often conflicting needs of customers. Customer research shows that retirees value flexibility and autonomy over their pensions. They want to be able to keep control of their money to fund still unclear retirement lifestyles or to pass on as part of their estate. However they also worry about running out of money during their lifetime, uncertain about how long the period of retirement will last and whether or not they will need to fund long term care later in their lives.

In order to offer value to customers, current retirement products on the market tend to serve a subset of these competing needs. Drawdown products provide flexibility on how much can be taken out, and when, as well as returning any remaining fund on death. At the other end of the spectrum, annuity products provide guarantees on the level of income and how long it will be paid for but have no flexibility if plans or health circumstances change.

While no new product fulfilling all these needs has yet been launched, many are seeing a two phased retirement solution as the answer - with an initial period of drawdown followed by an annuity purchase later in retirement when lifestyle and health are more settled. This would provide the customer with the longevity protection in the long run whilst still leaving them with flexibility in the short term.

However this solution means that the customer is exposed to significant investment risk in the drawdown phase. Sequencing risk (i.e. the risk of lower investment returns in early years when the fund is largest combined with drawing income from the fund) can have a significant impact on the amount of income a pensioner ends up receiving from their pension pot. As drawdown providers turn their attention to designing investment strategies suitable for a larger drawdown market, we are starting to see an increasing interest in the role that protected funds could play in post-retirement investment strategies. These types of funds, which are more common in the US, are currently mainly being used in the UK by a small number of life companies as a capital efficient way of providing guarantees in variable annuity style products. However, there could be scope to extend their use to more standard drawdown products.

What are protected funds?

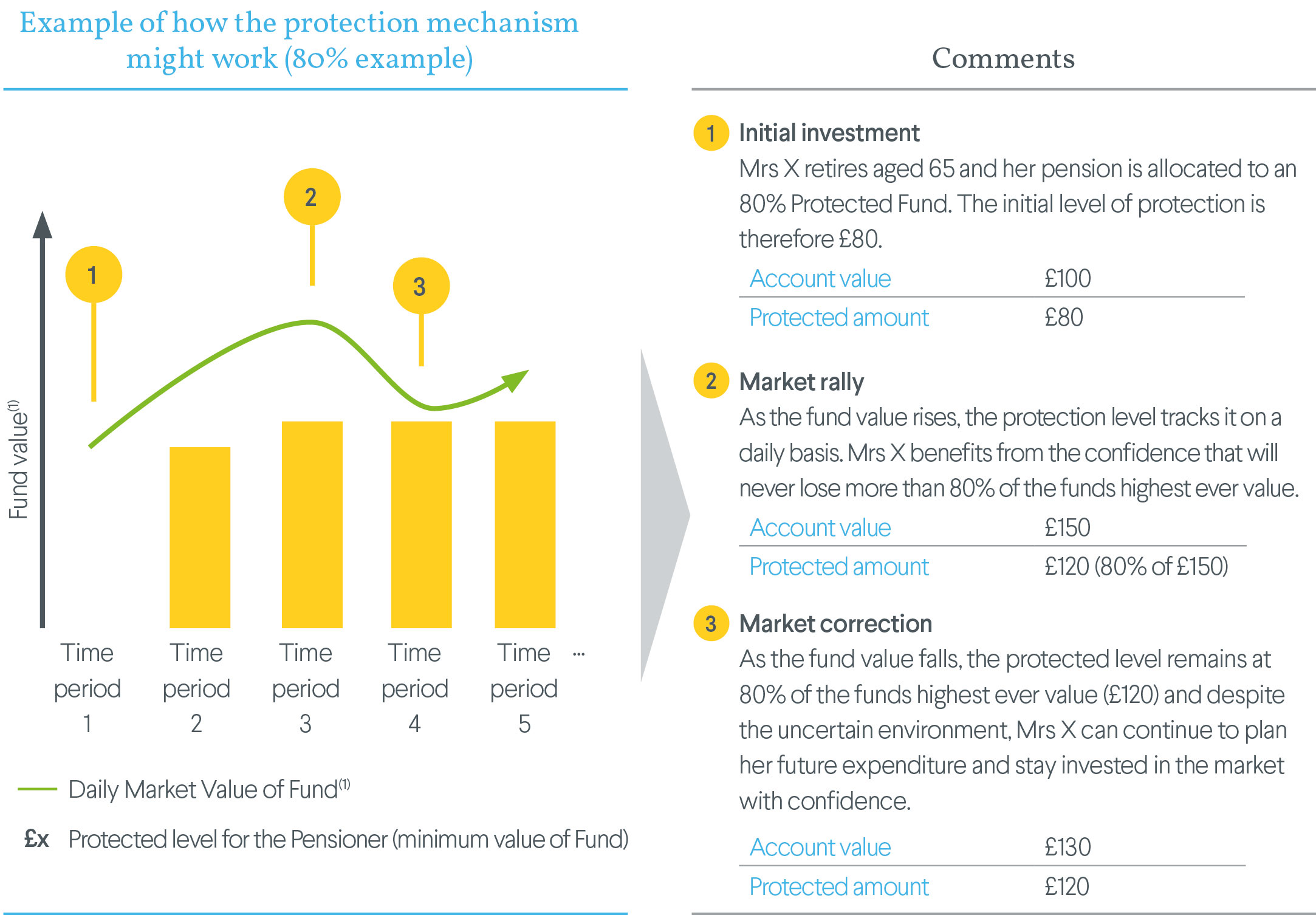

There are many different types of protected funds but at a high level they provide a guarantee that the fund value will never fall below a specified level. A common structure uses a CPPI (Constant Proportion Portfolio Insurance) mechanism to automatically re-balancing the fund, on a daily basis, between an investment asset and a defensive asset (usually cash). If the value of the investment asset starts to fall the fund starts to invest more in the defensive asset. As the fund value increases the protected amount can increase, thereby ‘locking in’ good investment returns.

The value of protected funds in drawdown

In order to assess the viability of using protected funds in drawdown we carried out analysis comparing different CPPI style fund structures with more traditional drawdown investment strategies. This analysis involved projecting forward the various investment strategies under thousands of possible economic scenarios allowing for different withdrawal patterns. Some of the key observations from this analysis were:

- A significant driver of the performance of the investment strategy is the level of management and other fund charges. Funds with high charges need to be truly generating higher returns in order to offset the charges and offer value to customers. Whilst protected funds are usually seen as a more costly option due to the cost of providing the guarantees, structuring protection around passively managed funds means that the total charges for management and protection on these funds can be brought to a level similar to that of actively managed non-protected funds.

- Investment strategies for drawdown tend to be fairly conservative, with customers typically investing in low to medium risk diversified growth funds in order to protect against downside market risk. The re-balancing mechanism of the protected funds modelled means that the investment part of the strategy, in which the customer is initially mainly invested, can be placed in higher risk assets. Our modelling showed that an 80% level of protection on a passive equity fund gave similar expected outcomes and a similar risk profile to an actively managed medium risk diversified growth fund.

- The protected fund structures modelled give a ‘hard guarantee’ in comparison to the non-protected funds likely performance in market downturn. This means that there is more certainty about how these funds will act in extreme market conditions which customers and their advisors may find reassuring, particularly in the context of sequencing risk.

- In the past, protected funds have been criticised due to the possibility of becoming cash-locked in a market downturn, i.e. the fund can move to be fully invested in the defensive asset with no chance of re-risking. Our modelling showed that this is a possibility and did happen in a small percentage of the projected economic scenarios. Customers and advisors investing in these funds need to be aware of this possibility and need to be able to take appropriate action in such scenarios occur. As such we would view online tools in the drawdown market to be key to the success of these funds. Such tools would allow easy monitoring of funds, potentially with inbuilt triggers to flag if the exposure to the investment asset has fallen below a threshold.

The retirement products market has seen significant change over the last few years and we expect this to continue as providers look to capture share of the growing defined contribution retirement market. This is likely to take the form of new products, new investment strategies – potentially including protected funds, and harnessing new technologies to give pensioners visibility and control over their investments.

Contributing Authors: