Deriving benefits from Remediation

04 Nov 2020

Over recent years we have seen increased regulatory attention on the fair treatment of customers; especially regarding long term products such as with-profits, unit-linked investments and banking products. The regulator has previously investigated and sometimes even fined firms where they have been found to breach the Financial Conduct Authority's Principles or Conduct of Business rules. Although there are significant financial, operational and reputational costs for firms being investigated there can be significant upside when firms actively rectify mistakes.

When you make a mistake, there are only three things you should ever do about it: admit it, learn from it, and don’t repeat it.” Paul ‘Bear’ Bryant

The need for remediation

There have been some recent high-profile examples of the industry’s failure for transparency and accuracy of advice, which has led to stricter oversight from the regulator and changes to disclosures. A secondary impact has been a regression in trust among the public towards the financial services. More regulatory pressure and thematic reviews into the financial services practices have raised red flags for the industry’s past and current practices. The conduct of life insurers has been under the regulator’s microscope, by either refining guidance, examining industry practice or investigating firms behaviour. Although these investigations may not always lead to a fine, they do place unfavorable attention at firms, taking focus and energy from the insurer’s strategic objectives. Mark Steward, FCA Executive Director of Enforcement and Market Oversight reiterated in a speech1 earlier this year that the regulator will impose tougher sanctions to firms that fail to correct identified breaches but also be more sympathetic firms which take pro-active, rapid and co-operative steps to redress customers by reducing sanctions.

Problems with delivery

Remediation can be complex and lengthy to deliver, requiring time and resources to be diverted away from other projects. It involves various parts of the business: legacy admin systems, product management, sales channels, legal, compliance and finance while ensuring board oversight of decision making across teams; something that can be challenging to accomplish. Methodology and outcomes will need to be clearly documented and efficiently communicated to stakeholders: shareholders, the regulator, policyholders and consumer groups. The regulator will weigh up the nature of the breach, its impact and duration and may scrutinise the proposed approach, stepping in to demand changes if required. It is crucial for firms to get it right the first time to avoid fines and to resolve the breach in a timely way. Customer complaints will need to be re-examined, by listening to calls and reviewing communication to ensure that the course of action is fair to customers. Communications to customer will need to openly, clearly and honestly explain the impact of remediation to the policyholder while considering all possible scenarios.

Benefits to firms

Firms proactively identifying their mistakes and taking steps to rectify them can reduce their operational risk and avoid regulatory intervention. Complaints, sometimes requiring FOS arbitration can be a significant expense for insurers requiring specialist handling teams. Remediation, if done right, can protect or even enhance the firm’s reputation and reduce complaints. Given the customer engagement is framed in the right way it can also improve persistency thus increasing the value of the book. The firm can also benefit from learning from past mistakes and improving the processes going forward to mitigate future errors.

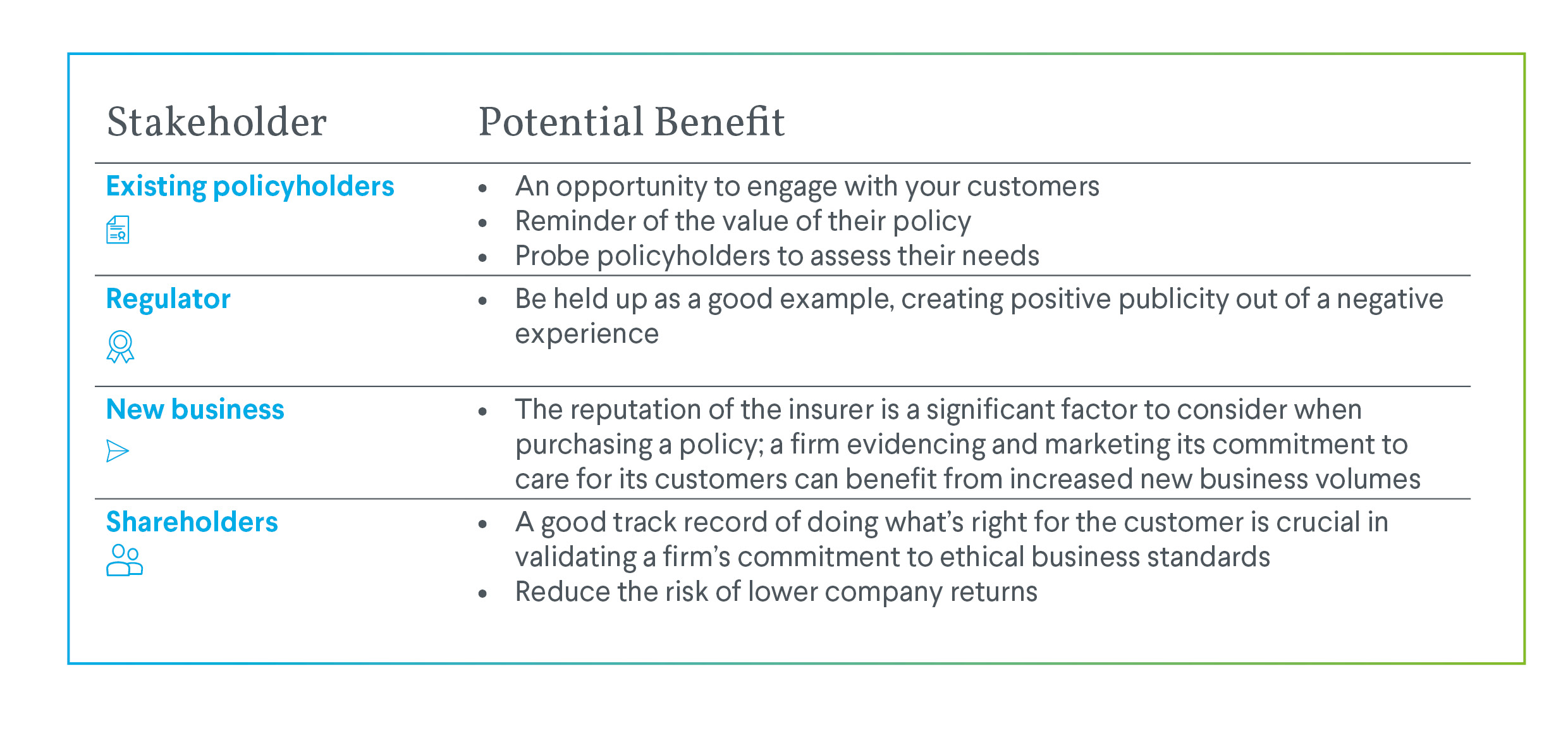

There can be secondary benefits too:

(Click on image to enlarge)

COVID-19

The current pandemic has forced firms to be very agile in adapting their existing product features or processes. Teams may have had to react quickly to customer situations with flexible approaches which existing administration systems may have struggled to cope with. Unfortunately, this can lead to errors and we observed a broader example of this in the current crisis where using legacy systems hastily meant the loss of nearly 16,000 coronavirus cases by Public Health England due to the use of an outdated Excel spreadsheet version to collate information from several sources.

For insurers, the pressure of responding quickly to change could lead to an increased risk of errors or administration issues. Firms will want to proactively tackle any issues that might arise and review any Covid related adjustments and changes in systems. Regular reviews of ongoing processes is more important than ever to check for potential problems before they escalate and require remediation or regulatory intervention.

Conclusion

As an industry, there are steps to be taken to improve the public’s confidence. A well run remediation exercise, not only fixes the underlying issues but can also be a fantastic way to show commitment to good customer outcomes and build ongoing engagement. An analysis of what went wrong can also help to guide a business to adopt more robust processes to help avoid further problems.

How Hymans Robertson can support you

Hymans Robertson has experience in independently validating and improving calculations, methodology and approach to meet regulatory standards. We can assist by using our actuarial expertise to build customer redress tools for mis-sold products or where calculation issues have arisen. We have helped firms in the past to respond to regulatory changes that require clear customer communications.

Collectively, our team has knowledge of a wide variety of financial services products, both for insurers and banks.

0 comments on this post