Fair treatment of vulnerable customers

In February 2021, the Financial Conduct Authority (“FCA”) released their finalised guidance FG21/1 on the fair treatment of vulnerable customers. This finalised guidance builds on the previous consultation GC20/3 and the key messages have remained largely unchanged.

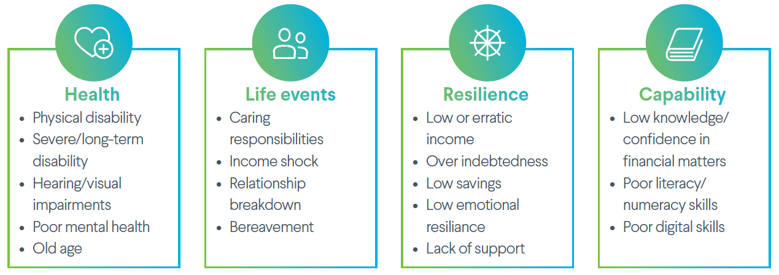

The guidance considers who vulnerable customers are and states that there are four key drivers of vulnerability. These four drivers and example characteristics associated with these drivers are shown below.

The FCA’s guidance covers four main areas, summarised as follows:

-

Understanding the needs of vulnerable customers – firms should consider the scale of vulnerability within their target market and understand how vulnerability can impact customer needs.

-

Skills and capability of staff – firms should ensure staff understand how their role impacts the fair treatment of vulnerable customers and are trained in how to identify vulnerable customers and can respond appropriately to their needs.

-

Taking practical action – firms should ensure the needs of vulnerable consumers are considered in product and service design, customer service and communications.

-

Monitoring and evaluation – firms should implement processes to evaluate and monitor whether they have met the needs of vulnerable customers.

Financial Lives Survey 2020

The FCA also recently published the results of its Financial Lives Survey 2020. The FCA carry out an annual survey with UK consumers to better understand their needs, attitudes towards financial products and interactions with financial services firms. The FCA’s Financial Lives 2020 survey also aimed to understand the impact of COVID-19 on customers. The results show an increased number of customers who display vulnerability characteristics and highlights the importance of firms getting to grips with FG21/1.

The impact of COVID-19 on vulnerable customers

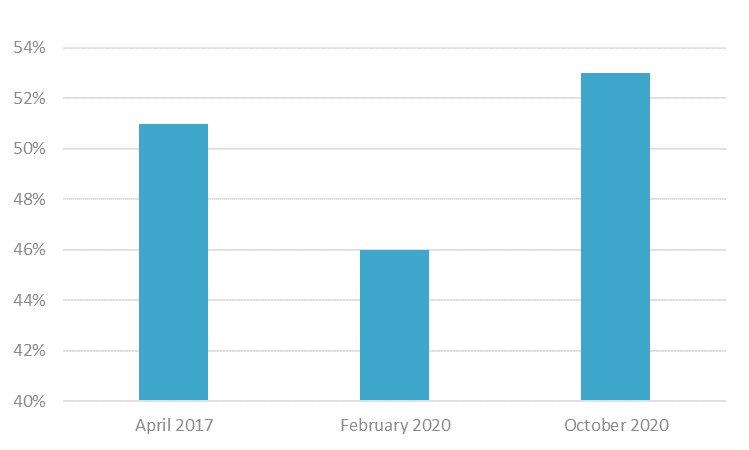

Between April 2017 and February 2020, there had been a slight downward trend in the number of customers who displayed vulnerability characteristics. However, between February 2020 and October 2020, the pandemic reversed this trend and resulted in an increase in the number of customers who displayed vulnerability characteristics, as shown in the graph below.

In the following sections, we take a look at the four vulnerability drivers and some examples of how the pandemic has affected these.

Health

The FCA Financial Lives Survey 2020 suggests that the pandemic has had a significant impact on consumers’ mental health. In October 2020, nearly 20%1 of consumers said they had a mental health condition or illness. This was nearly a 50% increase in the proportion of consumers with a mental health condition compared to February 2020. Those with poor mental health can often face difficulties when interacting with financial services. For example, 37%1 of those with a mental health condition are anxious to shop around for financial products and 56%1 said they found it difficult to interact with financial services providers. This puts these individuals at risk of misunderstanding products, purchasing products which don’t best suit their needs and reducing their potential protection and benefits.

Life events

As expected, the proportion of adults who have experienced a negative life event (such as an income shock, bereavement, or ill health) in the last year has increased significantly to nearly 30%1 of adults in October 2020. This was a 45%1 increase on the proportion in February 2020. The most common life event experienced was individuals being forced to work reduced hours. This may have resulted in reduced income, individuals being forced to use their savings and therefore reduced financial resilience. This is discussed further in the following section.

Resilience

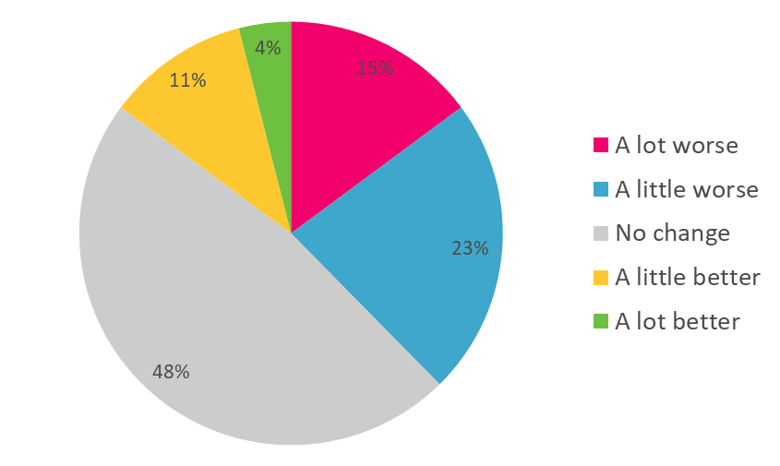

The impact of Covid-19 on adults’ overall financial situation is shown in the pie chart below.

Nearly 40%1 of adults’ felt their overall financial situation had worsened following the pandemic.

It is estimated that the proportion of UK adults with low financial resilience increased to nearly 30%1 in October 2020. This is a 35%1 increase on the proportion in February 2020 and an additional 3.5 million adults in the UK now have low financial resilience.

The FCA Financial Lives Survey 2020 estimates that 6%1 of adults have cancelled an insurance or protection policy since the end of February due to reduced affordability, leading to a small increase in the number of consumers without protection. Of those who cancelled a policy, the most common types of policy were home, travel and life insurance.

Capability

COVID-19 and national lockdowns have resulted in a huge increase in the use of digital services. For example, in October 2020, 28%1 of adults said that they had used online banking more frequently since COVID-19. This may create concerns around vulnerable customers, such as the elderly, who are less familiar with using online services. Their lack of familiarity and knowledge of online processes may make them more prone to scams. Almost half of UK adults1 say they have experienced unsolicited approaches about investments, retirement planning or pensions which could have been a scam since February 2020.

Conclusion

The FCA’s Financial Lives Survey 2020 shows that, as a result of the pandemic, over half of the UK population now displays vulnerability characteristics. The fair treatment of vulnerable customers is therefore an area which could affect the majority of customers. It is important that insurers spend time understanding the FCA’s recent guidance and embed the fair treatment of vulnerable customers across their business.

How Hymans Robertson can support you

Hymans Robertson has a wealth of experience in product design, regulation and managing conduct risk. We can provide support to ensure you treat vulnerable customers fairly and improve customer outcomes. If you wish to discuss this further, please do get in touch.

1 https://www.fca.org.uk/publication/research/financial-lives-survey-2020.pdf

This blog is based upon our understanding of events as at 9 March 2021. It is a general summary of topical matters and should not be regarded as financial advice. It should not be considered a substitute for professional advice on specific circumstances and objectives. Where this blog refers to legal matters please note that Hymans Robertson LLP is not qualified to provide legal opinion and therefore you may wish to obtain independent legal advice to consider any relevant law and/or regulation.