Letter to Work and Pensions Select Committee suggests three measures to solve the issue

State auto-enrolment credits should be introduced to reduce the Gender Pension Gap

18 May 2022

The Government should introduce State auto-enrolment credits for career breaks and radically change the framework of occupational pensions to reduce the inequality of the widening Gender Pension Gap, Chris Noon, Partner at leading pensions consultancy Hymans Robertson, has stated in an open letter to the Work and Pensions Select Committee. He has outlined his thoughts in the letter following his appearance to give evidence at the Committee’s “saving for later life” discussion.

The letter calls for the introduction of State auto-enrolment credits and highlights that this could be made in conjunction with two, more widely supported, measures - substantially reducing the AE earnings threshold to include more women on lower/part-time salaries and removing the offset to qualifying earnings in AE to pension from the first £1.

Auto-enrolment contribution credits would be similar to the way that the Government provides State Pension credits for certain individuals. These contributions could be made annually based on a notional earnings level. For example, if notional earnings were set at £16,240, the Government would pay an auto-enrolment contribution of around £800 a year (i.e. 8% x (£16,240 - £6,240)). This approach is analogous to State Pension accrual and reflects the fact that individuals in these situations (e.g. caring for children and/or elderly relatives) are adding value to society.

Explaining the arguments laid out in the letter, Chris says:

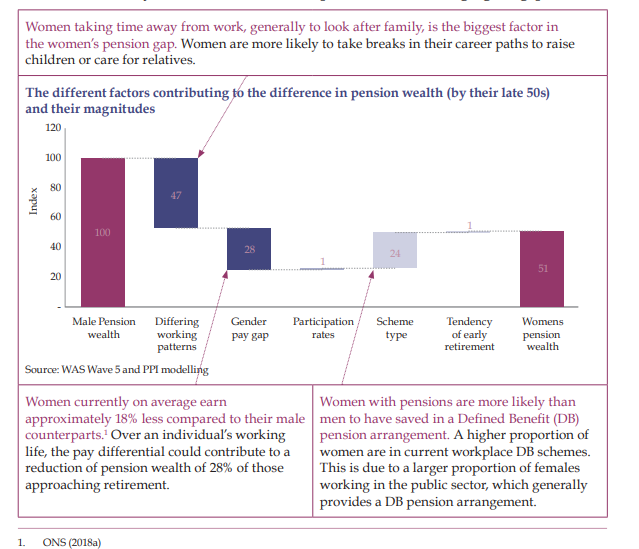

“It’s becoming increasingly clear that one of the primary shortcomings with the UK pensions framework is in the retirement outcomes for women, compared to those enjoyed by men. Evidence from the Pensions Policy Institute shows that this is largely due to the significant career breaks that many women take, as well as the higher prevalence of women working part time1. Introducing State auto-enrolment credits, alongside other measures to extend auto-enrolment, would make a significant difference in addressing the inequality.

“Figures in a House of Common’s Library briefing on auto-enrolment2 published in February suggests that reducing the auto-enrolment threshold from £10k to £5k would bring over 800,000 individuals into the scope of auto-enrolment. Of these, around three quarters of them (i.e. over 600,000 individuals) would be women.

“In our letter to the Select Committee we outline these three key measures which, if introduced to auto-enrolment, would serve to level the playing field and begin to close the chasm. The government simply can’t ignore this inequality which is blatantly unfair to millions of women.”

The letter explains:

A further House of Common’s Library Gender Pension Gap research brief3 from April identifies the primary drivers for this gap being so much larger than the Gender Pay Gap. The breaks many women take for caring responsibilities, and the prevalence of women working part time lead to significant periods where no private pension is accrued because:

- Career breaks are unpaid, meaning that no employer exists to make auto-enrolment contributions;

- The £10,000 auto-enrolment threshold means that working part-time (e.g. post caring or holding more than one part-time job) results in no pension contributions being made (unless the individual “opts-in”); and

- Not calculating pension contributions from the first £1 of income has a disproportionate impact on the savings of lower paid individuals.

Addressing these three shortcomings will help to significantly close the Gender Pension Gap. As discussed at the committee hearings, our view on how these shortcomings are addressed is as follows:

- Career breaks: The Government should provide auto-enrolment contribution for individuals in this situation, reflecting the value they are adding to society. These contributions could be made annually based on a notional earnings level.

- Auto-enrolment earnings threshold: This should be substantially reduced to bring significantly more people into automatic enrolment.

- Pensioning from the first £1: Removing the offset to qualifying earnings (i.e. £6,240). Employees can ultimately opt-out if affordability is an issue. While this has already been recommended by the Government it would need to be introduced in conjunction with the other two measures to have any real impact on the Gender Pension Gap.

1 PPI Understanding the Gender Pension Gap Report - July 2019

1 PPI Understanding the Gender Pension Gap Report - July 2019

2 Pensions: automatic enrolment - current issues (Page 31)

0 comments on this post