A funding boost but a collateral headache?

21 Mar 2022

Over the last decade (and more), interest rates on the whole have been falling, which has proved to be a funding headwind for almost all DB pension schemes. However, on the plus side it has boosted the available collateral within LDI portfolios which has helped with cashflow management as many schemes over the same period have tipped into cashflow negative status. The liquidity provided by cash in LDI collateral pools has provided a low cost, quick way of meeting cashflow demands for benefit payments etc in recent years.

However, 2021 saw the first signs of a reversal of that trend with interest rates rising and Central Banks sending clear signals of plans to meaningfully raise interest rates further in 2022. Whilst this has provided a helpful tailwind for funding, it has also reduced available collateral and Trustees are now having to start thinking about other means of raising cash. In instances where funding has risen sufficiently, de-risking may be a timely option to release cash. Where this isn’t the case, more careful planning and rebalancing may be needed to raise the cash required either to replenish LDI collateral or to directly meet cash outflow needs.

So far in 2022, further interest rate rises have also been coupled with rising inflation. Therefore, in the near term at least, the pressure on LDI collateral pools may have eased a little. That said, the latest rate rise in the UK was announced on 17 March, which will see UK interest rates increase from 0.5% to 0.75% in a bid to stem rising inflation. If rates continue to rise and inflation stabilises, or even falls, this is likely to be a double whammy tailwind for funding but also put collateral pools under increasing pressure. Trustees of DB schemes should therefore use this time to stress test their collateral pool to ensure that there is an acceptable level of resilience and inform early warning indicators for further action.

Stress Testing

The below table provides an example of how stress testing can be used to estimate the impact on LDI collateral due to movements in interest rates and inflation.

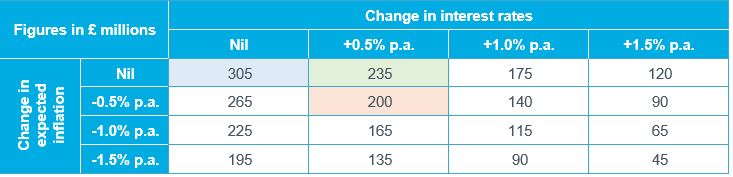

Collateral Stress Test

In this example, there is £305m (blue shaded) available collateral today. If interest rates were to rise 0.5% (on average, across all maturities), the available collateral would fall to £235m (green shaded). If this coincided with a 0.5% drop in inflation (a 1% real rate rise), the available collateral would drop to £200m (orange shaded). In this 1% real rate rise scenario, the collateral availability would reduce by £105m, or 1/3rd of the existing pool.

LDI managers should be monitoring available collateral on a daily basis and will have thresholds beyond which they will become less comfortable and request a cash top-up. It is important to understand what these thresholds are and what could take a scheme closer to those thresholds e.g. interest rate rises, inflation falls, cash withdrawal to meet scheme outgos etc. Contingency plans should then be put in place to ensure there isn’t the need for a forced sale of non-LDI assets or a forced unwinding of hedging positions to balance the books and meet scheme expenditure obligations.

And the point is...

There is a balance to be struck in all of this though. Utilising leverage within LDI portfolios has been a great de-risking tool, enabling higher liability hedge ratios to be achieved whilst not having to sell growth assets and give up return. And more often than not, interest rates and inflation tend to move in similar directions, with offsetting impacts on collateral levels. So, my point here is not about introducing huge amounts of prudence into the collateral sufficiency pool, but rather to flag the importance of:

- Understanding the proximity to leverage limits and hence collateral calls

- Understanding the cashflow needs, and the impact that it could have on leverage levels even if interest rates and inflation don’t move

- Having a process in place for being able to top-up collateral when needed to avoid being forced to sell non-LDI assets at a potentially inopportune time or unwind hedging (which is essentially re-risking)

If you have any questions on anything covered in this blog, please get in touch.

0 comments on this post